Oman's Renewable Energy Boom – Solar, Green Hydrogen, and Grid Upgrades "Three Arrows in One"

- Matthew Deng

- 24 hours ago

- 5 min read

Oman, a country that once quietly contributed to the global energy map as an oil producer, is transforming at an unprecedented pace and scale into a leading "green power" player in the Middle East. This is more than just an energy structure adjustment—it's a profound economic transformation driven by national strategy, massive investments, and full-chain industrial layout.

Grand Blueprint: Market Explosion Driven by National Strategy

Oman's renewable energy development features a clear and ambitious top-level design, sending strong signals to global investors:

Net-Zero by 2050: Oman has committed to achieving net-zero emissions by 2050.

2030 Mid-Term Target: Aim to reach 30% renewable energy in total electricity demand by 2030, with installed capacity exceeding 8 GW.

National Champion Leading the Way: State-owned OQ Alternative Energy (OQAE) is designated as the "national champion," responsible for developing industrial and B2B green projects. OQAE expects its renewable portfolio to surpass 10 GW by 2030.

Accelerated Investments: OQAE plans to reach Final Investment Decision (FID) on nearly 2 GW of new renewable projects (primarily solar PV) by the end of this year.

Electricity Market and Organization

Oman's electricity market remains highly centralized and vertically integrated under utility dominance, but the Independent Power Producer (IPP) model introduces competition and private sector investment.

Regulators and Government Entities

Authority for Public Services Regulation (APSR): Oversees the entire electricity sector, issuing regulations and technical guidelines.

Nama Power and Water Procurement Company (NPWP / Nama PWP): The core of Oman's power market, acting as the sole national off-taker. It plans future generation and water capacity and procures new IPP/IWP projects via competitive tenders.

Nama Group: A state-owned conglomerate with subsidiaries covering all links in the power supply chain.

IPP Model on the Generation Side

Composition: Generation includes Nama Generation and numerous other IPPs.

Operation: Most large-scale projects (including renewables like Ibri II, Manah I & II) are built and operated via IPP mode. Private consortia bid for projects and sign long-term Power Purchase Agreements (PPAs) with Nama PWP for stable revenue.

I-REC Market: Nama PWP periodically auctions International Renewable Energy Certificates (I-REC), enabling companies to participate in promoting renewable consumption. For example, the Dhofar Wind Project is the first in the GCC registered under I-REC standards.

Market Characteristics Summary

High concentration dominated by state-owned Nama Group and subsidiaries.

New generation capacity primarily introduced through IPP/IWP to attract private investment.

Nama PWP's procurement and planning serve as the core indicator of market direction.

Electricity Tariff Structure Background

Oman's electricity tariffs are regulated by APSR and implemented by entities like Nama PWP. Recent reforms focus on:

Phased Subsidy Removal: Gradually adjusting tariffs to reflect true costs for economic sustainability.

User Differentiation: Separate structures for residential, commercial/industrial, and large industrial users.

Residential Tariff

Tiered pricing: Progressive rates where higher consumption means higher per-kWh costs.

Subsidies Retained: For Omani households, partial subsidies remain, often with low base rates or free allowances.

Expatriate Tariffs: Higher rates for foreign residents and second homes, with minimal or no subsidies.

Industrial & Commercial Tariff

Higher Pricing: Focus of subsidy removal, making rates higher than subsidized residential.

Two-Part Tariff: For large industrial users—Energy Charge (based on kWh) + Demand Charge (based on peak demand in kW or MVA).

Flagship Projects: Solar, Wind, and Integrated Solar-Storage

Oman's energy growth centers on large-scale IPPs, actively incorporating storage for grid stability.

Large-Scale Solar IPPs: Capacity Release in Waves

Ibri II: Oman's first utility-scale PV project (500 MW), operational since 2021.

Manah I & II: Combined 1,000 MW, expected to commence commercial operations in the first half of 2025.

Ibri III IPP: 500 MW, awarded to a Masdar-led consortium. Oman's first utility-scale PV with integrated storage, planned for 2027 commissioning.

Wind Power and Diversification

Operational: Dhofar Wind Farm (50 MW, commissioned 2019).

Future Pipeline: About 1 GW of wind projects advancing across regions. Under-construction Rawafid Projects include Riyah-1 and Riyah-2 (total 234 MW) for PDO oil fields. Planned for 2027: Duqm Wind IPP (234-270 MW) and Al Wusta Governorate Wind IPP (Mahoot I, 342-400 MW).

Green Hydrogen: Building a Localized Green Energy Ecosystem

Oman's strategic depth lies in deeply integrating energy transition with economic diversification and local industrial chains.

Green Hydrogen as a "Super Driver"

OQAE co-develops multiple large green hydrogen projects.

Massive Solar-Storage Pairing: Supporting "Green Hydrogen Oman" and similar projects with up to 25 GW of dedicated renewable capacity—driving super-large solar-storage buildouts.

$1.6 Billion! Building the Middle East's Largest Polysilicon Factory

Under construction in Sohar Free Zone: A $1.6 billion polysilicon manufacturing plant, set to become the region's largest.

Massive Capacity: Once fully operational, it will supply polysilicon for 40 GW of annual solar module production.

Multi-Party Financing: Oman Arab Bank ($2.2 billion agreement), IFC (up to $2.5 billion loan), Future Fund Oman ($1.56 billion support).

Professional Challenges and Rooftop PV Potential Analysis

Dust and High Temperatures: "Derating" Impacts

Desert climate challenges PV performance via heat and dust: High temperatures reduce efficiency, with performance ratios (PR) lower in summer across test sites.

Dust Evidence: In Muscat PV plants, 7.5% soiling causes ~5.6% monthly generation loss; 12.5% soiling leads to ~10.8% loss.

Opportunity: Huge market for cleaning robots, as regular cleaning significantly boosts annual yield.

Rooftop PV: A Massive Untapped Market

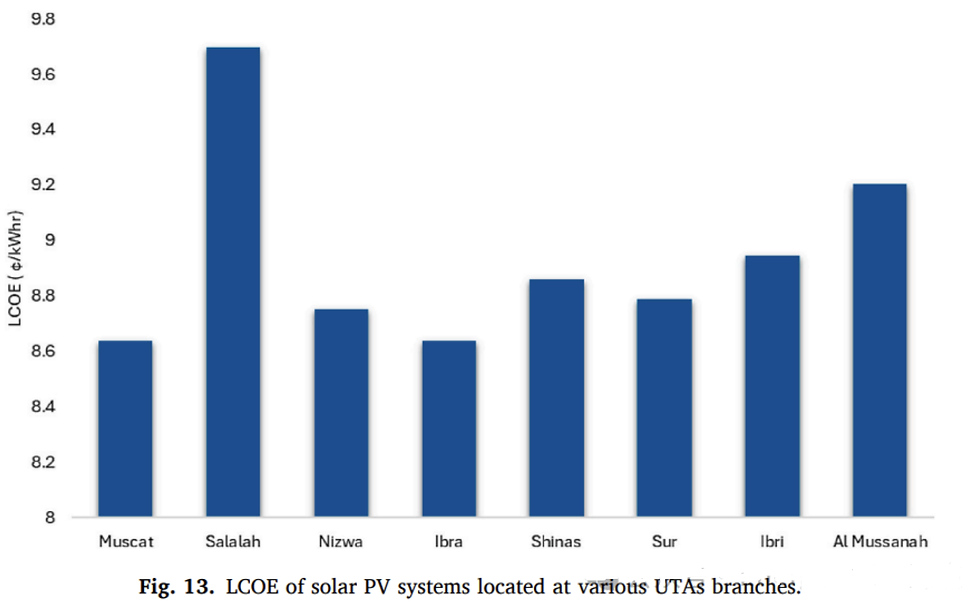

Best Regions: Northern areas (especially Ibri) offer the highest AC generation.

LCOE Outlook: Most sites range from 8.5 to 9.7 US cents/kWh.

Oman's PV sector is in the early stages of large-scale development. Current LCOE around 8.5 cents/kWh is close to or slightly better than natural gas true costs but far above global lows of 1-3 cents/kWh in the Middle East. True potential lies in massive "catch-up" room. With 2 GW to 10 GW projects landing, economies of scale will rapidly drive LCOE down, establishing future competitive advantages in power costs.

Policy Bottleneck: Despite 95% residential installation willingness, Oman currently lacks strong rooftop PV promotion policies. However, with accelerating government renewable investments, robust policies like Feed-in Tariffs (FiT), net metering, and subsidies are expected soon.

Through national will, capital leverage, and industrial focus, Oman is positioning itself as a strategic hub for green energy in the Middle East and globally. This full-chain layout transforms it from an energy consumer into a future green energy manufacturer and exporter.

If you're exploring opportunities in Oman's booming renewable sector—particularly with durable solar panels, integrated energy storage solutions to combat dust/heat challenges, and reliable systems for utility-scale, rooftop, or green hydrogen-linked projects—Kada Energy is your ideal partner.

As a Tier 1 solar value chain expert operating in 46+ countries, Kada Energy delivers beautiful, customized, cost-effective solutions, including advanced storage for Solar Home Systems and Green Mini Grids in emerging markets. Their expertise aligns perfectly with Oman's shift toward resilient, high-performance renewables that address intermittency, soiling, and long-duration needs. Contact Kada Energy for tailored strategies to capture this explosive growth: visit us.

Comments